NAR Reports Show Now Is a Great Time to Sell!

/

We all realize that the best time to sell anything is when demand is high and the supply of that item is limited. The last two major reports issued by the National Association of Realtors (NAR) revealed information that suggests that now continues to be a great time to sell your house.

Let’s look at the data covered by the latest Pending Home Sales Report and Existing Home Sales Report.

THE PENDING HOME SALES REPORT

The report announced that pending home sales (homes going into contract) are up 2.4% over last year, and have increased year-over-year now for 22 of the last 25 consecutive months.

Lawrence Yun, NAR’s Chief Economist, had this to say:

"The one major predicament in the housing market is without a doubt the painfully low levels of housing inventory in much of the country. It's leading to home prices outpacing wages, properties selling a lot quicker than a year ago and the home search for many prospective buyers being highly competitive and drawn out because of a shortage of listings at affordable prices."

Takeaway: Demand for housing will continue throughout the end of 2016 and into 2017. The seasonal slowdown often felt in the winter months did not occur last winter and shows no signs of returning this year.

THE EXISTING HOME SALES REPORT

The most important data point revealed in the report was not sales, but was instead the inventory of homes for sale (supply). The report explained:

- Total housing inventory rose 1.5% to 2.04 million homes available for sale

- That represents a 4.5-month supply at the current sales pace

- Unsold inventory is 6.8% lower than a year ago, marking the 16thconsecutive month with year-over-year declines

There were two more interesting comments made by Yun in the report:

"Inventory has been extremely tight all year and is unlikely to improve now that the seasonal decline in listings is about to kick in. Unfortunately, there won't be much relief from new home construction, which continues to be grossly inadequate in relation to demand."

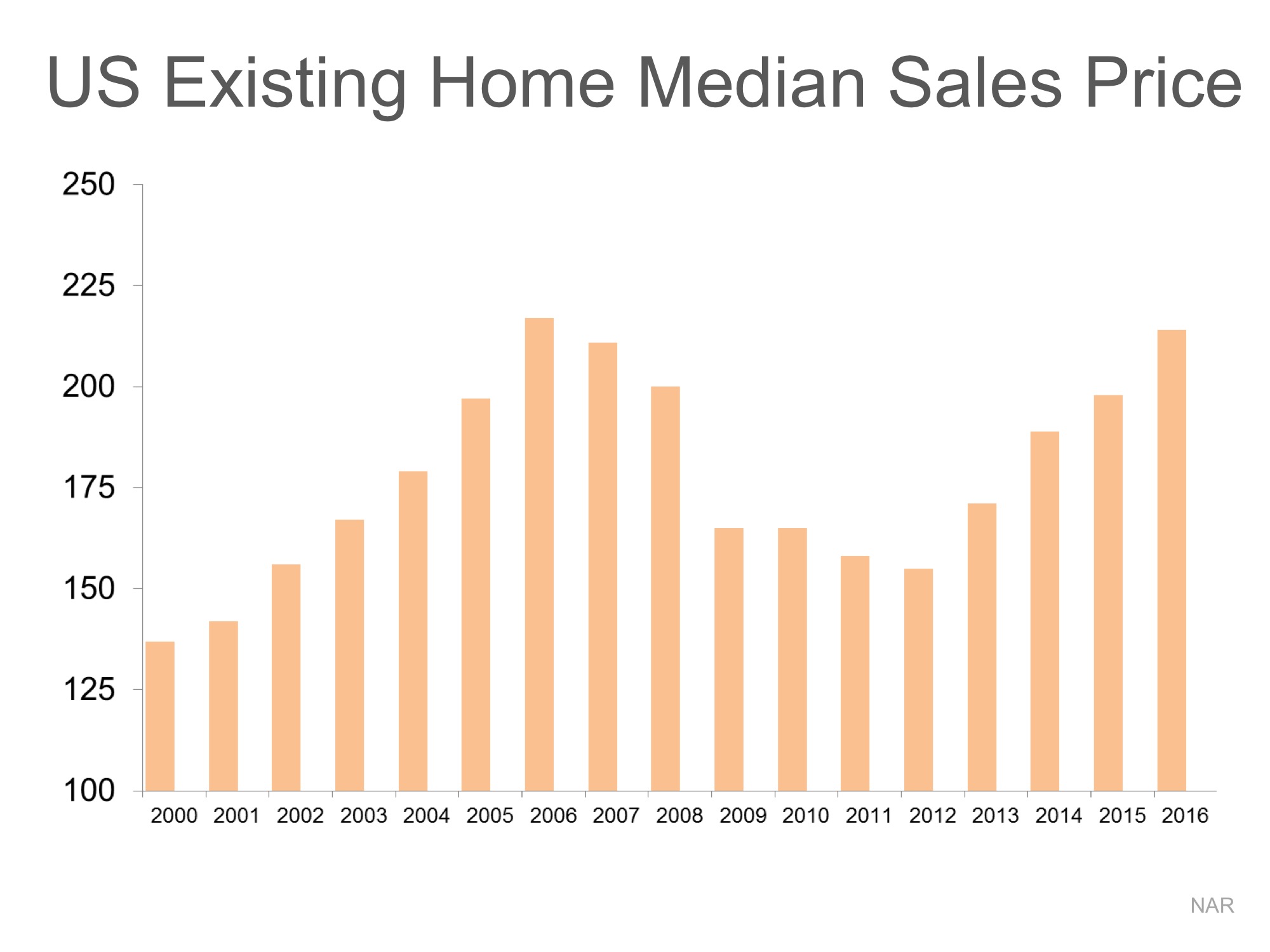

In real estate, there is a guideline that often applies; when there is less than a 6-month supply of inventory available, we are in a seller’s market and we will see appreciation. Between 6-7 months is a neutral market, where prices will increase at the rate of inflation. More than a 7-month supply means we are in a buyer’s market and should expect depreciation in home values. As Yun notes, we are, and will remain, in a seller’s market with prices still increasing unless more listings come to the market.

"There's hope the leap in sales to first-time buyers can stick through the rest of the year and into next spring. The market fundamentals — primarily consistent job gains and affordable mortgage rates — are there for the steady rise in first-timers needed to finally reverse the decline in the homeownership rate."

Takeaway: Inventory of homes for sale is still well below the 6-month supply needed for a normal market. Prices will continue to rise if a ‘sizable’ supply does not enter the market.

Bottom Line

If you are going to sell, now may be the time to take advantage of the ready, willing, and able buyers that are still out looking for your house.